Bridging the Access Gap in Financial Services

Despite the rapid digitization of financial services, over 1.4 billion adults globally remain unbanked. In emerging markets, this challenge is even more visible — limited documentation, low financial literacy, and a deep-seated distrust of formal institutions continue to exclude millions from basic financial tools.

Take India, for instance. Digital payments crossed the ₹100 trillion milestone in 2023, yet only around 100 million people actively use credit cards — just a fraction of the population. Similar trends are playing out across Southeast Asia and Africa, where mobile usage has exploded, but formal credit adoption remains low.

This digitally underserved population isn’t hard to reach — they’re simply underserved by traditional models.

Where Do We Begin? Rethinking Issuance

To bring meaningful financial inclusion, issuers must rethink how they design and deliver products. And that begins by choosing the right issuance model: Prepaid, Credit, or BNPL — depending on the user’s profile, onboarding needs, and risk appetite.

1. Why Product Fit Matters

Each product serves a specific purpose, and for new-to-digital users, the starting point matters more than ever.

- – Prepaid cards offer ease of access and greater control — ideal for the financially cautious.

- – Credit cards provide flexibility but come with higher eligibility barriers.

- – BNPL gives users instant access, but can expose them to repayment stress without financial literacy.

The goal isn’t just access — it’s access on the user’s terms. That’s what drives trust, adoption, and long-term engagement.

2. What Should a Modern Issuance Platform Deliver?

Regardless of whether you’re a bank, fintech, or government body, an effective issuance platform should be:

- – Fast to launch with minimal tech overhead

- – Support both physical and virtual card issuance

- – Enable real-time provisioning and lifecycle management

- – Comes with built-in fraud prevention and security features like tokenization and 3DS

- – Be cloud-native or hybrid, to scale reliably

- – Ensure compliance, reporting, reconciliation, and KYC support

- – And most importantly — it should be modular and API-first

3. Prepaid, Credit, or BNPL — What Works for Whom?

For first-time users or those outside the formal banking system, prepaid becomes the most accessible entry point. It offers spending control without the complexities of repayment or risk assessment.

BNPL, on the other hand, works well in e-commerce or merchant ecosystems but needs responsible usage to avoid debt traps. Credit cards remain aspirational — and best introduced when users are financially ready.

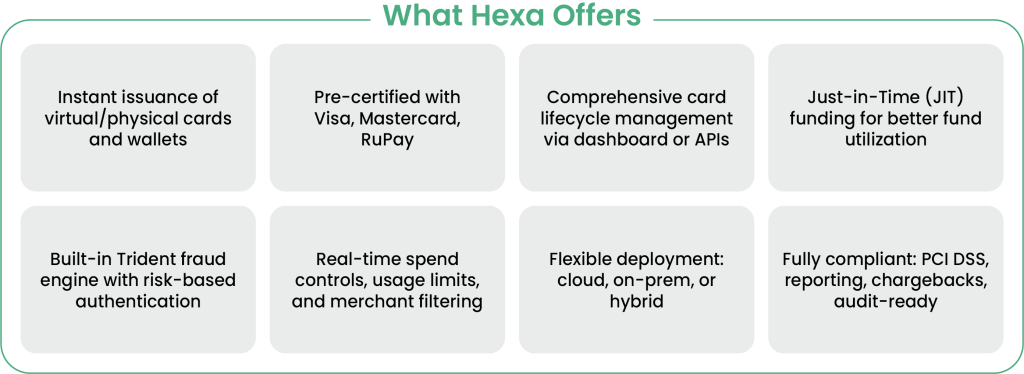

4. Spotlight: Wibmo’s Hexa Platform–

Enter Hexa — Wibmo’s end-to-end platform built to power inclusive issuance at scale.

It’s designed with the underserved in mind — combining speed, security, and scalability with complete configurability.

Important Use Cases–

Hexa supports a wide array of use cases that go beyond just payments:

From gig workers to employees, students to rural consumers — the platform adapts to your audience.

5. The Issuance Playbook: A Step-by-Step Approach

For issuers building for the underserved, here’s a phased approach to ensure success:

Know Your Audience – Who are you solving for: gig workers, students, migrants, rural users?

Choose the Right Model – Prepaid for access, BNPL for conversion, Credit for flexibility.

Pick a Capable Platform – Like Hexa, which offers:

- – Instant issuance

- – Pre-certified networks

- – Fraud control + lifecycle management

- – Developer-ready APIs

Go Live Faster – Use pre-built modules, test environments, and scalable infrastructure.

Optimize & Grow – Use real-time insights to improve UX and extend reach.

Build Trust – Clear communication, support, and feature transparency go a long way.

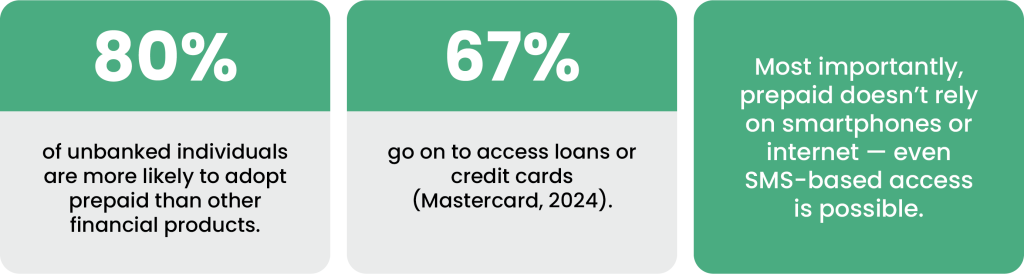

Why Prepaid is Emerging as the New Gateway

The global prepaid market is expected to grow from $3.6 trillion in 2024 to $21.46 trillion by 2034 (Precedence Research). Prepaid is no longer just an expense management tool — it’s becoming a starter financial identity.

For the underserved, this is not just a card. It’s a first step toward empowerment.

Final Word: Inclusion Starts With Issuance

Platforms like Hexa don’t just issue cards — they unlock trust, control, and access for those long excluded from the financial system.

The future of financial inclusion is already unfolding — it’s modular, mobile, secure, and increasingly, prepaid. If you’re looking to build for the underserved and drive meaningful change, we’d love to partner with you. Reach out to us at [email protected].